[ad_1]

Kathmandu, August 2. Judging from the indicators assessing the internal and external economic situation, there is no problem in Nepal’s economy.

Reasons such as inflation being controllable, no pressure on external balance, and weighted average lending rate falling back to single digits indicate that there are no problems with the economy.

Although below the target, the forecast released by the Central Statistics Office shows that economic growth will improve compared with the previous year. However, not only ordinary people but also the private sector have not directly felt the improvement in the economy.

In particular, data on imports and exports and credit flows to the private sector reveal the slack in the economy. Although growth in agriculture and services supported economic growth, data released by the Central Bureau of Statistics confirmed that domestic economic activities were not functioning normally due to negative growth in real sectors such as construction and production, with only normal growth in wholesale and retail tax rates.

The central bank acknowledged that there were problems in the construction sector due to the central bank’s facilitation through monetary policy.

In particular, government finances and a weak economy weighed on the health of the financial sector. The central bank also acknowledged that the crisis in the microfinance and cooperative sectors was putting further pressure on the economy.

Dr. Gunaka Bhat, head of economic research department of Nepal Rastra Bank, said that although economic activity has improved compared with the previous year, economic activity last year did not expand as expected.

Bhatt said there was no pressure on the external balance and no inflationary pressure. “There has been an increase in interest accruals. Credit growth in the private sector is below the target set by the state bank,” Bhatt said. “The solution can be found in the financial sector. However, it has not been used. Banks are waiting to invest. Banks should not invest irresponsibly as they have done before.”

Butt said the data showed that there were problems with the bank recovery and economic activity was not expanding as expected.

“The real economy sector is under pressure. Although the situation appears to be improving, expansion in the real sector (economic activity) is not expected,” he said. This suggests that the situation is improving.

Since there are no problems with prices and external relations, there is great pressure on the financial side. The increase in bank non-performing loans in the past two years shows pressure that has not been seen even after the earthquake and the COVID-19 pandemic.

Bankers said risks in the post-pandemic world are shifting and the impact of economic easing is affecting the banking sector. Despite ample liquidity in the banking system and falling interest rates, credit expansion was low for the second consecutive year.

The demand for loans is low due to the disappointment in the private sector. Banks do not seem to be adopting a credit expansion strategy. The banking sector is under pressure from deteriorating asset quality. Bankers say banks cannot adopt a credit expansion strategy even if they want to. When the banking sector is in trouble, there is a need to increase the “money supply” to make the economy run, which also affects the economy.

The National Bank has decided to use alternative sources of capital to relieve the pressure on the banking sector. However, financial experts said that under the pressure of increasing risky assets and loans, the banking industry cannot solve the problem unless it manages resources to increase capital.

Although there is no time to achieve price and external stability, experts believe that the economy can only accelerate if the problems in the financial sector are resolved.

Unrevised financial statements released by banks in mid-June showed some improvement in capital issues. If the central bank were to exercise some flexibility through monetary policy during this fiscal year, things would appear to be easier.

However, banks face challenges managing an increase of about $16 billion in non-bank assets in a year, which indicates that banks’ asset quality and financial stability are under pressure.

Bankers said that there are many problems with this type of loan, especially for small and medium-sized enterprises, because they have weak ability to repay loans. As the foundation of the economy, the problems of small and medium-sized enterprises are a major challenge facing the economy.

Banks are also under pressure as cooperative and microfinance problems grow. Although financial stability through liquidity is not a problem, deteriorating asset quality is becoming a risk for the financial sector.

Data from last year released by the central bank on Sunday before the monetary policy announcement also showed that although some sectors were very loose, the overall economic situation was not loose. The increase in remittances and services and the contraction in foreign trade led to a significant increase in the current account, current account balance and foreign exchange reserves.

Domestic economic activity has failed to increase, although external sector indicators provide a solid foundation for expansion of economic activity. Inflation is under control, and falling interest rates, ample investable resources in the banking sector, and strong external sector momentum provide a foundation for economic activity.

While most economic indicators were positive, slow credit flows to the private sector and pressure on government fiscal and import and export data pointed to weak economic activity.

Based on National Bank data Online NewsShows an economic picture:

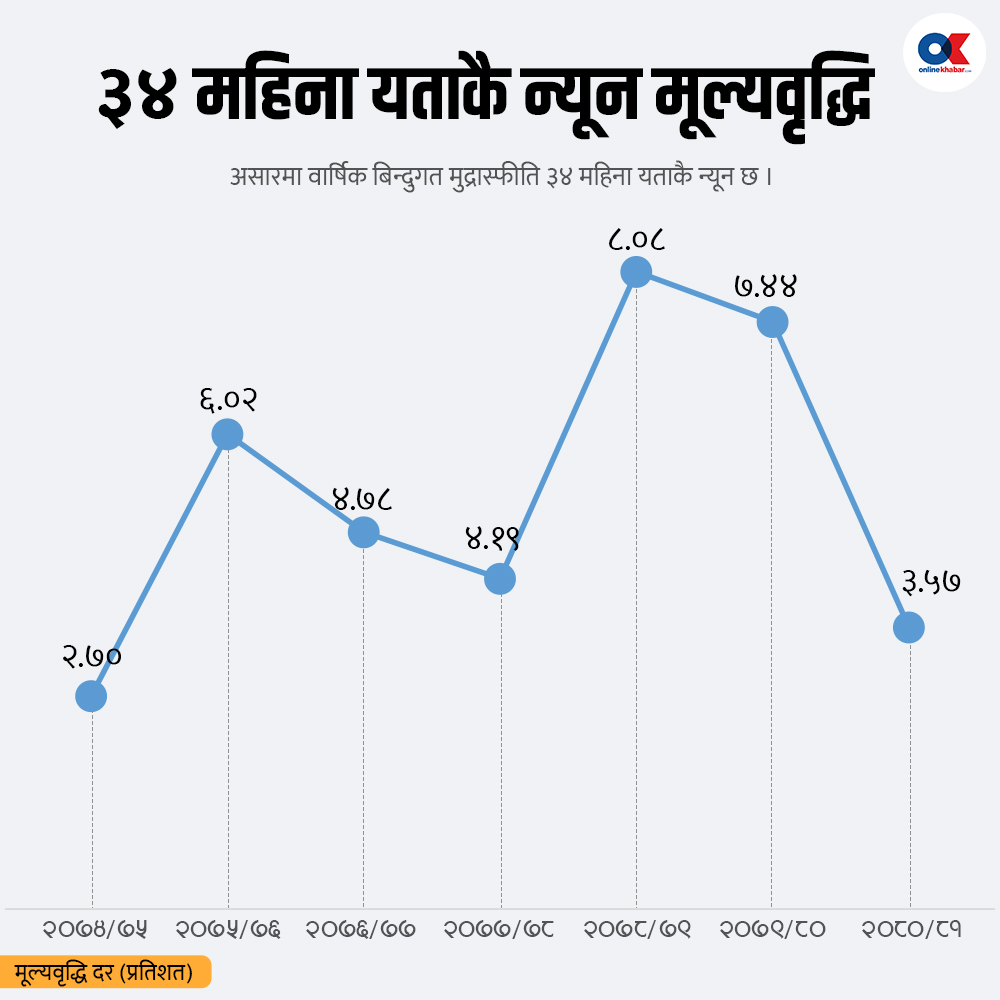

१. Inflation has remained high for the past two fiscal years and is within the monetary policy target range this year. The average inflation rate in 2078/79 was 6.32%, and in 2079/80 it was 7.74%, compared to 5.44% last year. Inflation seems to be under control in recent months. On an annual basis, the inflation rate at the end of June 2079 was 8.08%, and at the end of June 2080 it was 7.74%. In June 2081, the figure was 3.57%.

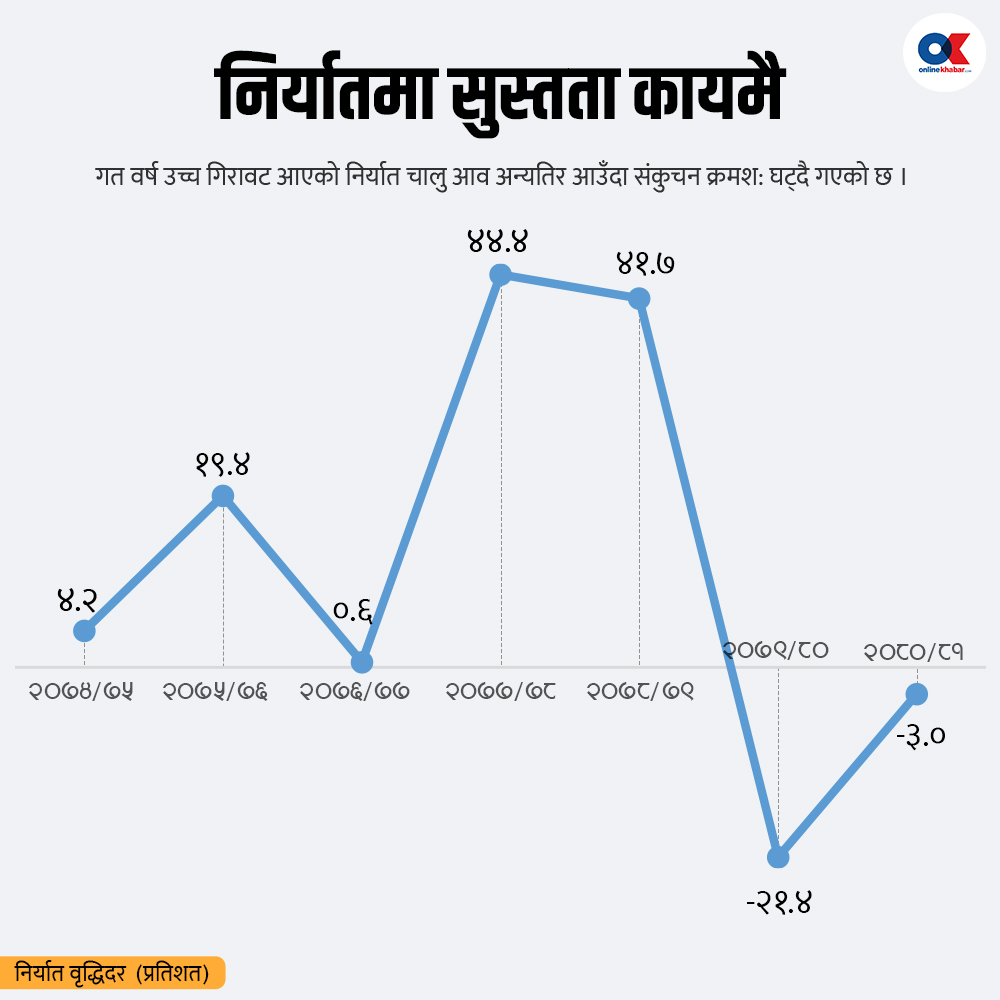

२. Export trade slowed for the second consecutive year. During and after the Covid-19 pandemic, exports grew by 44.4% and 41.7% in the 2077/78 and 2078/79 fiscal years, respectively, and fell by 21.4% in the 2079/80 fiscal year. Export trade fell by 3% last year.

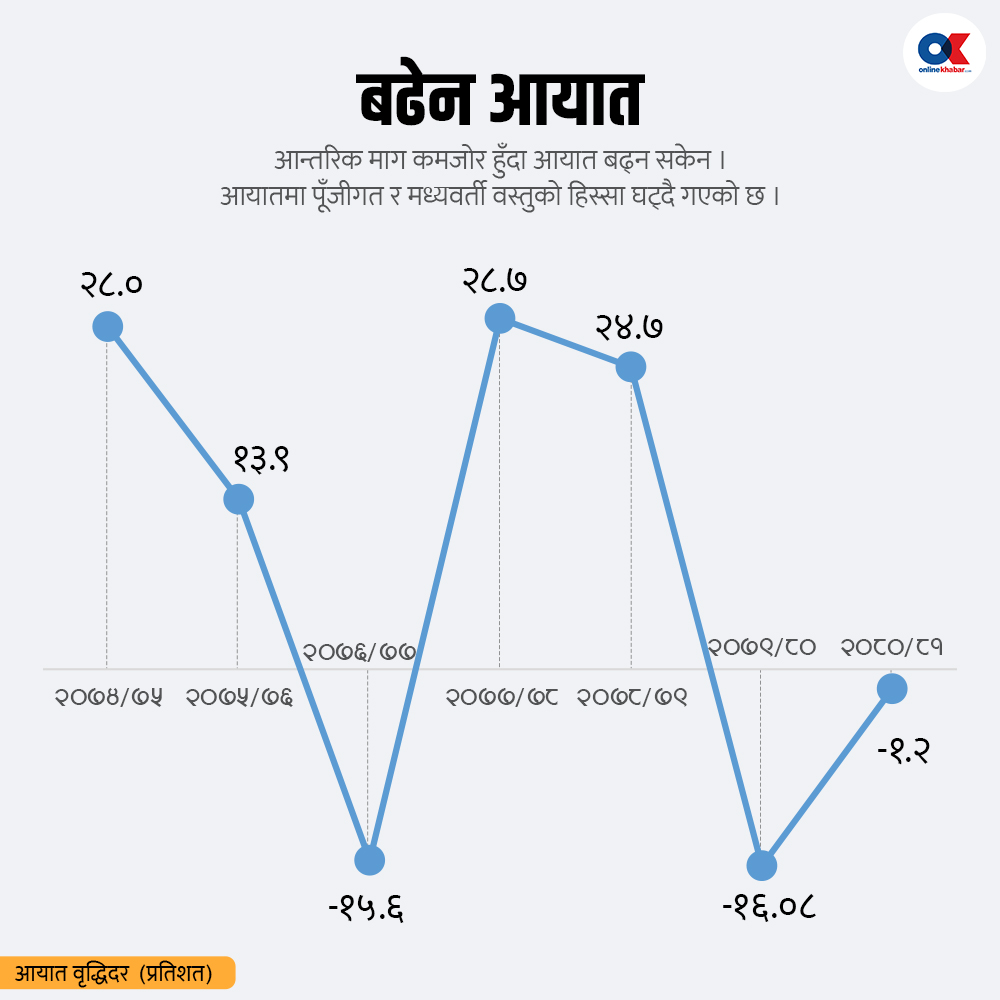

३. The same trend is seen in imports. This indicates weak domestic economic activity. Imports increased by 28.66% and 24.72% during and after the COVID-19 pandemic in 2077/78 and 2078/79, respectively, and fell by 16.1% in 2079/80. It fell by 1.2% last year. Flexible monetary policy and interest rate cuts in the post-pandemic period led to high credit expansion in the stock market, which led to high growth in real estate and the stock market. Economic capital gains have thus increased demand for consumer goods. Despite the increase in imports, the National Bank and the government have had to intervene in various ways to control imports. However, in the past two years, due to the sharp increase in the number of young people going abroad for employment and studying, the number of young people consuming has decreased, and although the number of tourists has increased slightly, the demand for young people has decreased. More people are going abroad because tourists have failed to increase demand. Due to cooperatives and microfinance problems that have led to payment problems for dairy farmers, the middle class has stopped spending from savings and how to manage their daily lives. Imports have also decreased due to the overall decrease in demand.

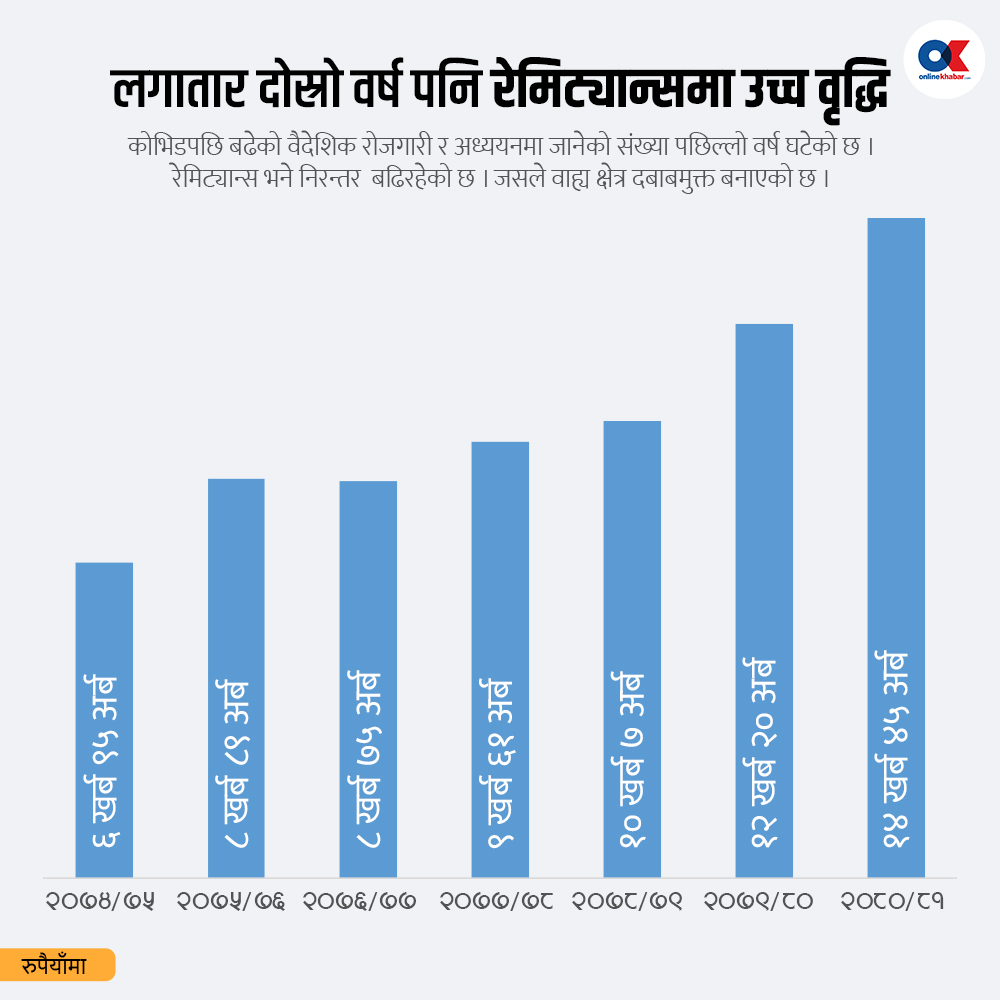

४. Despite the shrinking imports, remittances are high. Despite the doubts that foreign employment will be affected by the coronavirus and the Russian-Ukrainian war, on the contrary, remittances continue to grow at a high rate. In 2078/79, remittances grew normally, but in 2079/80 and last year, higher growth was seen. Last year, remittances reached 15 trillion, 45 billion, and 32 million. An increase of 16.5% over the previous year.

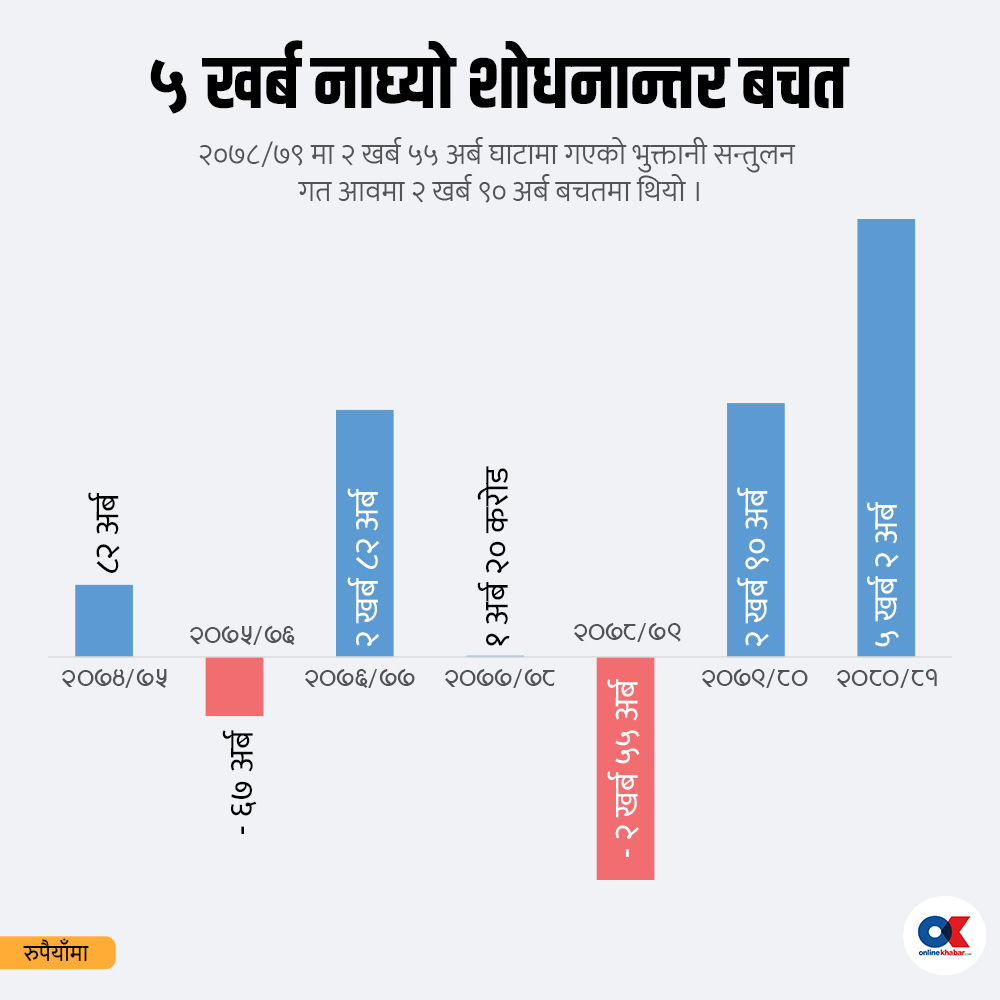

५. The balance of payments has reached a historical surplus due to increased remittances, reduced imports and improved services. Last year, the balance of payments was 5 trillion and the surplus was 2 billion. The current account balance also showed a surplus of 2 trillion and 21 billion.

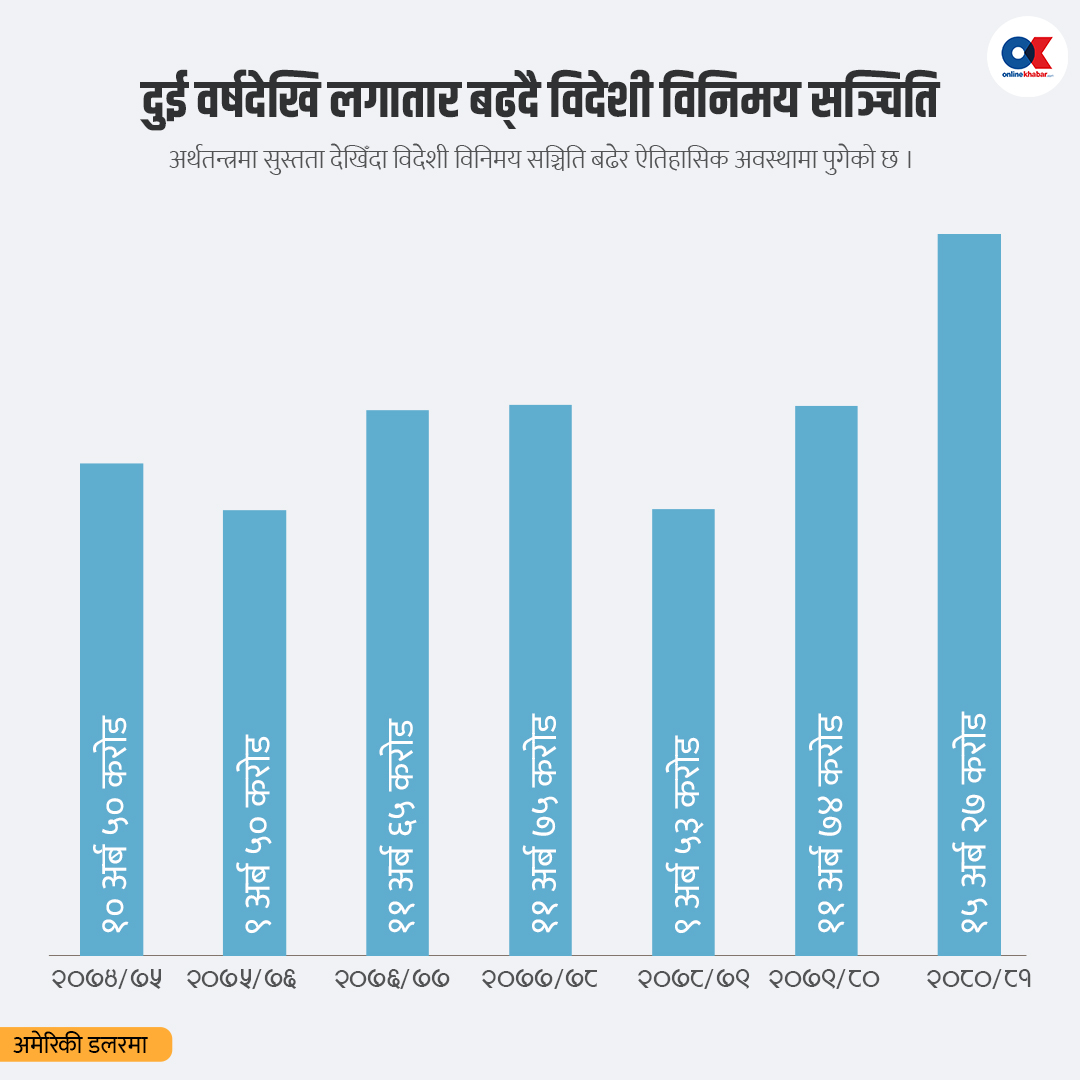

६. Foreign exchange reserves have reached a record high, as the situation of reduced imports and remittances has improved, although foreign direct investment, foreign grants and loans have not yet achieved the expected results. Foreign exchange reserves fell from $9.53 billion in June 2079 to $15.27 billion in June 2081. The increase in remittances and the positive impact of the service industry contributed to the growth of foreign exchange reserves. Among them, imports decreased, and foreign exchange reserves increased more. Experts said there is no reason to be too excited because of the increase in production without improvement.

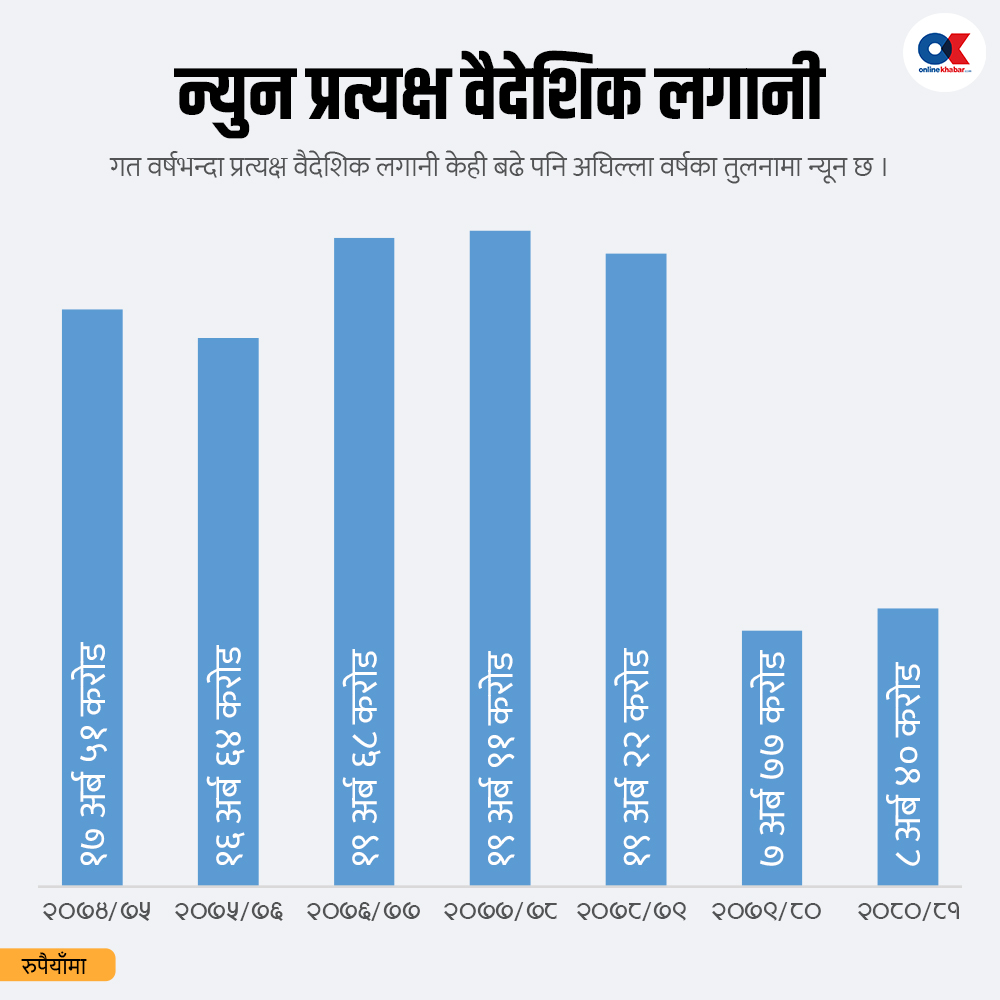

७. Foreign direct investment disappointed for the second year in a row. Compared to 2079/80, foreign direct investment improved last year, but it was still disappointing compared to the previous year. Net foreign direct investment, which had been close to $20 billion for the past few years, was only $7.777 billion in 2079/80 and only $8.44 billion last year.

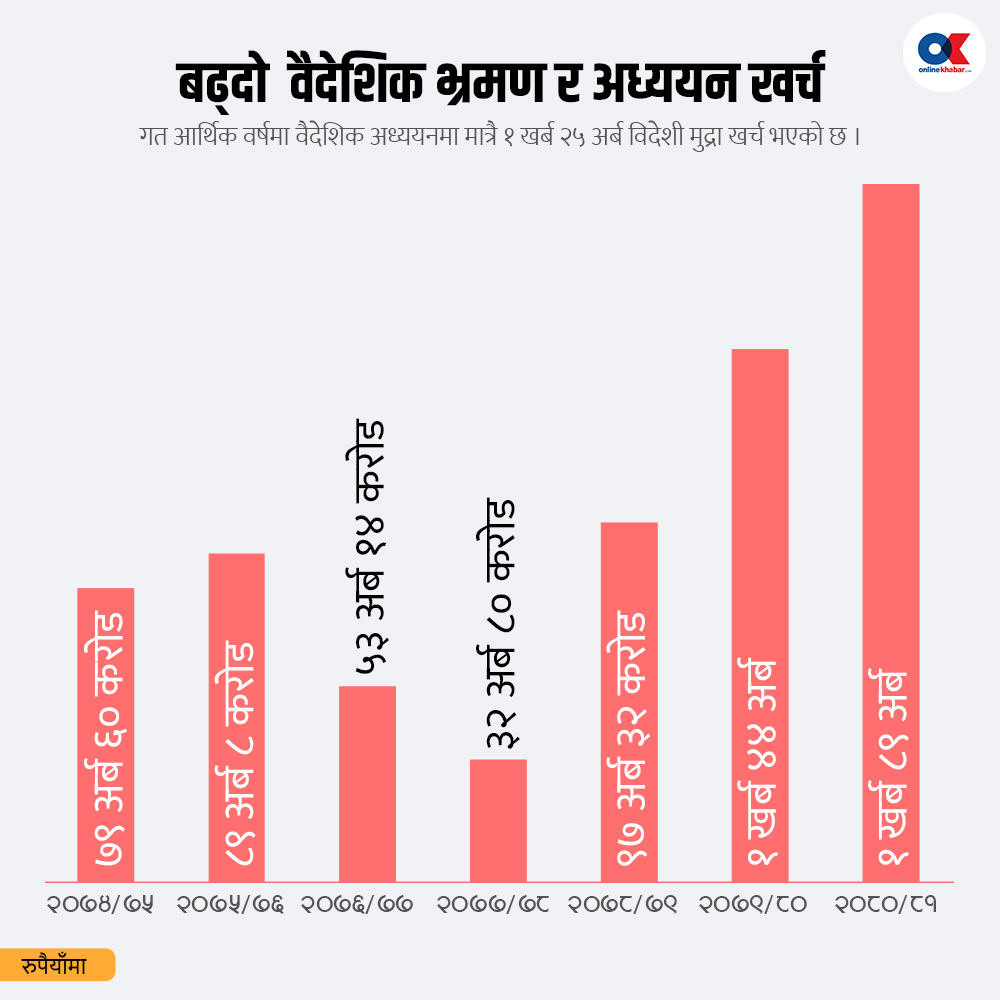

८. Despite a sharp increase in tourism and information technology revenues, the services account was in deficit due to the high cost of studying abroad. Last year, spending on studying abroad was only 1.25 trillion, while Nepal’s spending on tourism abroad reached 1.89 trillion. However, the net services revenue deficit declined.

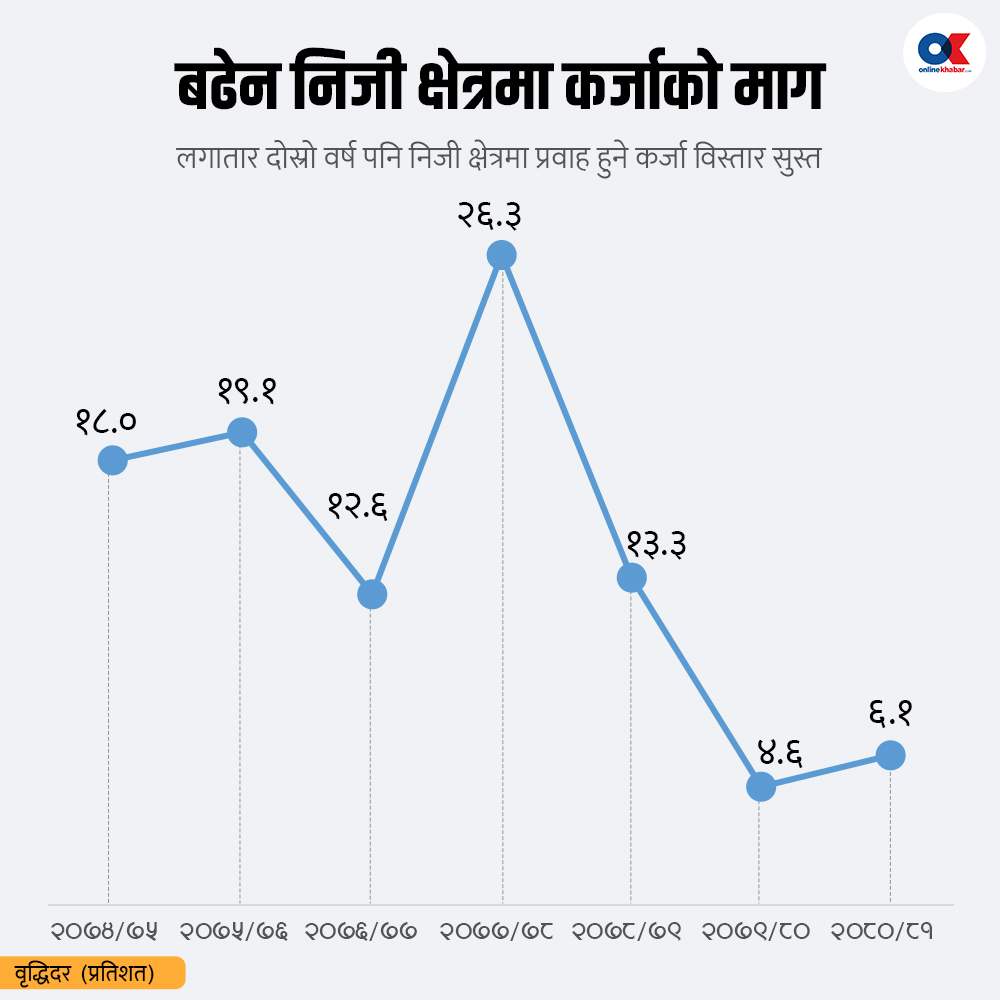

९. Even with the fall in interest rates, there is no demand for loans from the private sector. Nepal’s private sector credit growth was about 20% on average, but there has been a break since the last two years. Banks are unable to raise loans. This has led to increasing arrears in interest payments. This has increased the financial sector’s claims on the private sector to 6.1% in 2080/81. In 2079/80, such loans were only 4.6%. Despite the monetary policy’s credit expansion target of 11.5%, the financial sector’s interest rate has risen to 6.1%. The net credit expansion was only 5.8%. On the other hand, the monetary policy expected a 12% expansion in the broad money supply. It reached 13% by the end of the fiscal year.

१०. Interest rates have fallen to single digits. In the past, the private sector has said that the investment environment has deteriorated due to high interest rates, but even with the decline in interest rates, private sector enthusiasm and investment do not seem to have increased. The weighted average interest rate on loans fell from 13.03 percentage points in February 2079 to 9.93% in June 2081.

[ad_2]

Source link