")

")

[ad_1]

Monty Lacuson

Dear readers/followers,

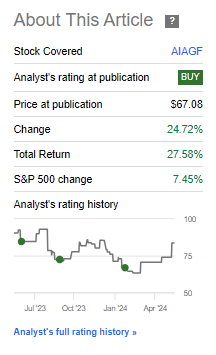

AurubisOTCPK:AIAGF)(OTCPK:AIAGY) is a company I’ve been following and investing in – and this investment, which is also the largest investment I have made in it, has finally paid off. In my previous article, you can Find my rating for this company here , with a Buy rating, and the results since then speak for themselves. You can also find the article here.

Finding Alpha Aurubis TSR (Look for the Alpha Aurubis TSR)

This isn’t my victory lap, though. Yes, the company has performed very well. But as you can see in the inset chart, I’ve stayed positive for much longer than that, and my performance has been subpar since then. The total return since my first post is still negative – even if it’s only 1%.

but I I believe the company has far more upside potential than you think – something I have been pointing out for a long time. In this article, we will look at the latest results to see what the company has done to correct operations and what further reversals we can expect as the company “struggles” upward. While my total position is now in the black, I expect much more from this company.

Let me tell you why.

What are the benefits of copper and recycling?

Despite the struggles in the basic materials and mining sectors, I still believe copper is a good sector to invest in – copper is a big feature of Aurubis. Many of the investments I make are cyclical and are facing a tough 2024-2025 period, but my time frame is much longer.

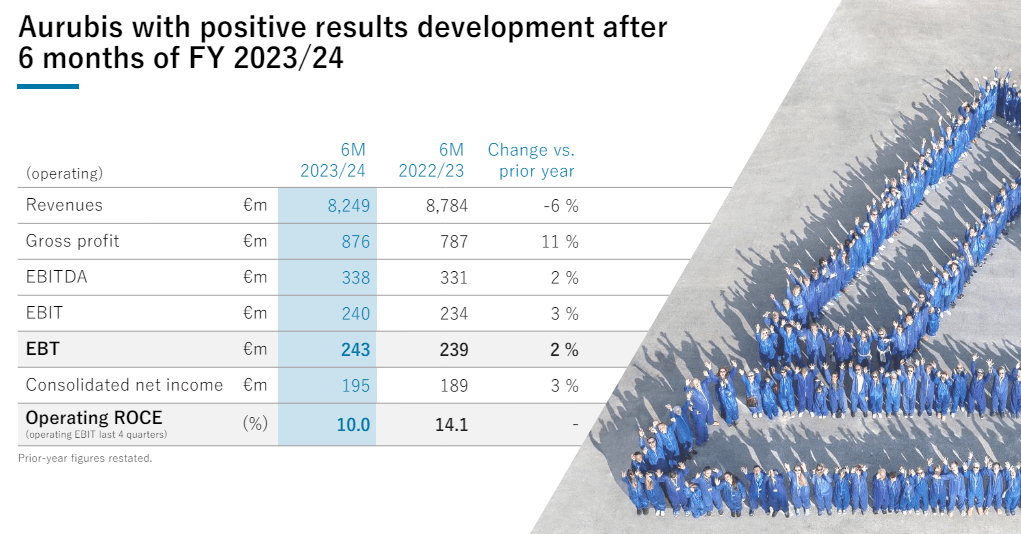

At this point, less than a month after the last report, we focus on the first six months of the year. Operating profit is up slightly, net cash flow is down, operating ROCE is down further – barely in the double digits at 10.0%, and full-year profit is expected to exceed nearly €500 million in 2023-2024.

Although the return on operating capital was lower, it was a positive overall. The reason for the EBT was better pricing of concentrate and copper premiums, a big increase in wire demand, and lower overall energy costs. I see utilities reporting lower energy costs, but that’s a negative. This shows that when you invest broadly like I do, one company’s disadvantage is another’s advantage. As long as energy costs remain low, Aurubis has some tailwinds here given the absolute energy consumption of its operations.

Infrared (Australian IR)

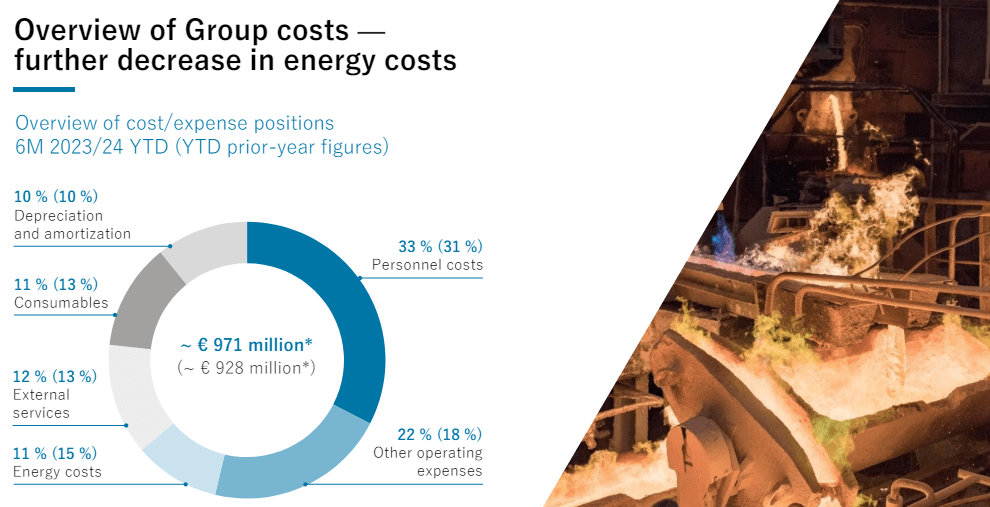

So there is a good reason to justify the stock’s recovery – the underlying business has recovered as well. The improved market conditions also include sulfuric acid, the company’s secondary product. The company’s gross margins have also improved, and once you look at the breakdown of the cost profile, the decline in energy costs becomes very clear. Energy costs have indeed fallen, while personnel and “other” costs have risen quite a bit.

Infrared (Australian IR)

I did some digging to understand what exactly the 4% increase in other operating expenses means, but haven’t found a good answer yet. There are several reasons why energy costs are falling, but the most important ones are lower electricity and natural gas prices, as well as more aggressive hedge management, which are leading to some significant upside here.

Like many German businesses, Aurubis also maintains low leverage and a very strong balance sheet. The company currently has a high equity ratio of 54.2% and a debt coverage ratio of 0.2x – meaning net financial debt as a percentage of 4Q EBITDA is high, which means leverage is very low indeed.

The company currently operates in two segments – Recycling and Smelting & Products. Most of the sub-segments in the first segment have declined and ROCE has fallen sharply. Unfortunately, Recycling is the reason for the decline in performance, because while Custom Smelting & Products has declined, EBIT and EBT have increased, while ROCE is still close to 15%.

For the full year, the company’s forecasts remain mixed, so we expect volatility to continue. To be clear, I do not expect valuations to improve materially this year, even though I am one of the only ones to expect earnings to come under further pressure. Reduced but ample concentrate supply forecasts, subdued recycling inputs due to increased competition in Asia (although most smelters are now on supply until 2024), less positive sulphuric acid revenue expectations, and wire rod remaining one of the only product categories with strong demand all combine to make the company’s potential in this area volatile. At a group level, ROCE will be below the company’s 15% target range at 10-14%, mainly due to negative trends in recycling that could see ROCE margins fall to 5%.

Current group guidance does imply higher 2024 EPS is possible, but that’s only compared to the dismal 2023 EPS we see, which is down 37% from 2022.

The reason I am optimistic about Aurubis is because of the long-term trend. I believe that we are in a situation where there will be an increase in business from recycled metals and from companies that supply these metals and have expertise in these areas.

Current forecasts are consistent with this, as Aurubis’ adjusted earnings are expected to grow over the next three years. Growing at a rate of nearly 10% per year (FAST chart source)

This is not a large company. Aurubis currently has a market cap of just over €3 billion, but the extremely low debt (less than 5% of long-term debt/capital) and growth potential, combined with solid fundamentals and operating history and expertise, make me a firm believer in the company’s long-term upside potential.

However, it is undeniable that there is a lot of volatility associated with this type of investment. The company does not always exceed or meet its expectations, it has failed to meet expectations more than 25% of the time, and more than 10-20% of the time depending on the time frame you look at. Therefore, investing in Aurubis requires that you are willing to take on risk in order to receive a decent return.

How “reasonable” a payout are we talking about, and within what time frame?

The stock is valued well and trading at less than 10 times earnings, leaving plenty of room for upside.

Despite outperforming the S&P 500 by 20% since my last article, the company actually still trades at less than 10x earnings. This is despite what I see as compelling upside to 2024-2026 earnings estimates.

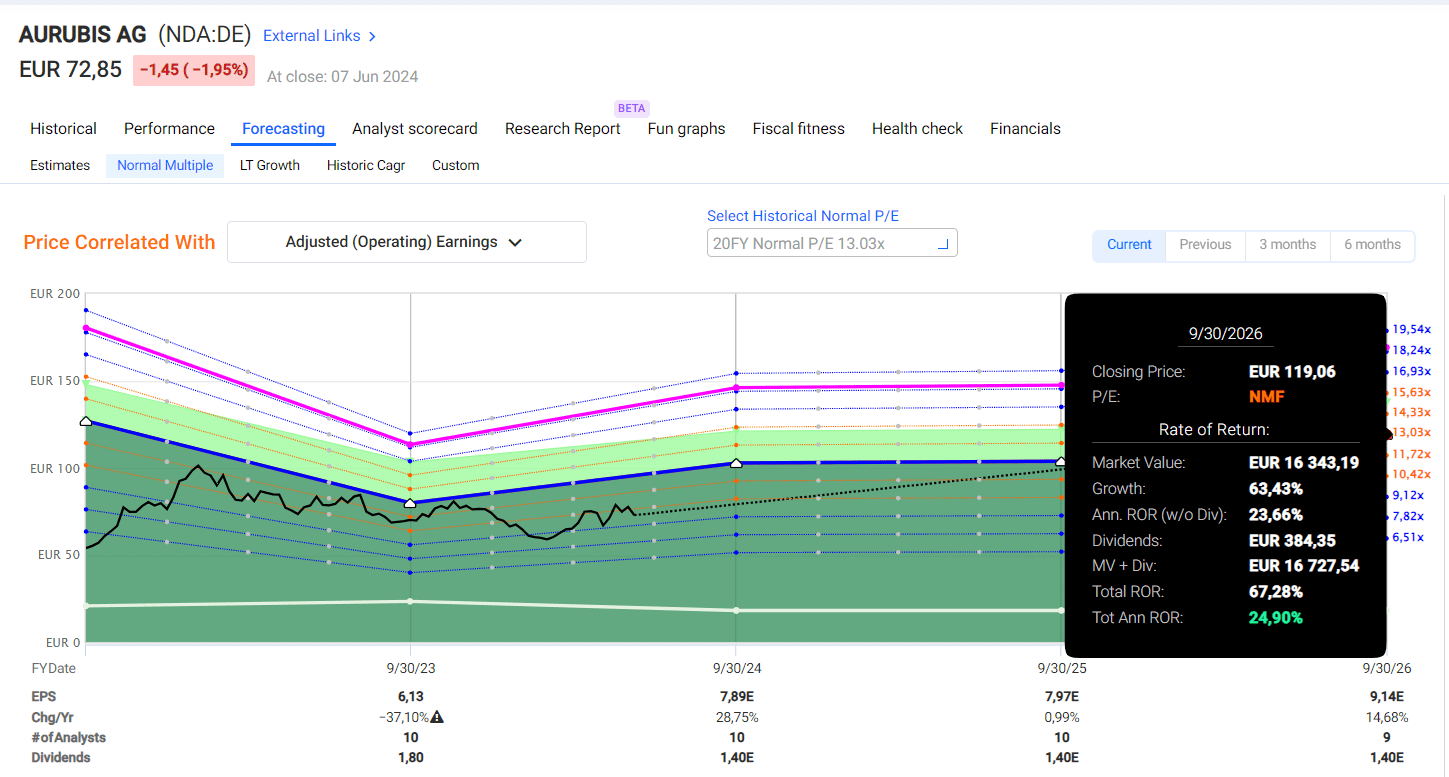

Current forecasts show the company growing earnings very quickly, with EPS increasing by 28.7% this fiscal year and EPS increasing by about 7% in 2025 and 2026. If this forecast comes true and we assign to the company its historical average (assuming 13x the 20-year average), the results would look like this.

Aurubis Upside Quick Chart (Aurubis Upside quick chart)

If you bought in at the same time as I did, the potential return would be in the triple digits. Even without that, a return of nearly 25% per year is still very good, although a dividend yield of less than 2% is not very attractive.

Aurubis is a complex investment and I don’t expect everyone to “get it all”. In fact, my own position is still a “work in progress” compared to my entire portfolio and is less than 0.5% of the total position. The last target price I gave in my last article was 80 euros per share, and it is now 72.8 euros. I will not change this target price here because I don’t believe or see us getting any improvement in clarity or forecasts, but I do think the company is indeed worth 80 euros per share, which represents a low standard P/E ratio of 10 for a company that will grow double digits.

Currently, S&P Global has a rating range of €61 to €110 per share for this company, with an average of €82 per share. 5 of the 9 analysts with a “buy” or similar positive rating expect Aurubis to achieve substantial overall growth in the company’s EBITDA over the next few years, with 2023, which we just passed, being the bottom or trough of the trend. This has been the case for the past two forecasts, with the PT changing only slightly as analysts have downgraded the company based on various scenarios. I personally do see downside potential in Aurubis – we could realistically see around €50-55 per share – at which point I would obviously add to my position significantly.

Risks and concerns?

I don’t see much changing other than macro factors. The company’s low leverage makes the underlying risk quite small. The company’s contract volume rises and falls. The main reason for the current downturn we are seeing is the stagnation of hamburger, which will obviously increase again.

The current situation is that Chinese smelters (especially those that buy concentrates, like Aurubis) and some international mining companies set prices specifically for the concentrate market (the market Aurubis operates in), and the benchmark price could be abolished and the business conditions for Aurubis, its customers and suppliers, would be very different. Currently, Aurubis is buying concentrates from more than 40 large mines around the world. These prices and sourcing patterns could change – but it is something that will have to be watched closely. If this were to happen, Aurubis would be far from the only company that would be affected. At the moment, this is a remote risk, but I think it is at least worth mentioning.

paper

- Aurubis is a market-leading German metallurgical company involved in copper, other non-ferrous and precious metals, and sulphuric acid by-products. The company has one of the most extensive expertise in this area in the world and it deserves far more attention than it is getting.

- As of the latest quarterly report, there is more clarity on certain expectations for 2024, I think more clarity than before. This allows us to act with more confidence and maintain our PT and positive stance on this company.

- I believe that Aurubis’ common shares are still a “buy” at or below 80 euros per share. I have looked at the company’s options, but do not consider them relevant at the moment due to the low premium.

Remember, I just want to say:

1. Buy undervalued companies at discounts (even if the undervaluation is small, not incredibly huge) and let them recover over time, reaping both capital gains and dividends.

2. If the company performs far beyond the norm and becomes overvalued, I will take the gains and move my position into other undervalued stocks, repeating point 1.

3. If the company is not overvalued, but is hovering within a reasonable value range, or falling back to an undervalued level, I will buy more if time permits.

4. I will reinvest earnings from dividends, savings from work, or other cash inflows as described in point 1.

Here are my criteria and how the company meets them:Italic).

- The overall quality of this company is high.

- This company is fundamentally safe/conservative and well run.

- The company pays an adequate dividend.

- This company is currently cheap.

- The company has realistic upside based on earnings growth or multiple expansion/reversion.

There are still enough positives here, and I also now think the company is getting closer to being a “bargain.”

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Editor’s Note: The securities discussed in this article do not trade on major U.S. exchanges. Be aware of the risks associated with these stocks.

[ad_2]

Source link