[ad_1]

Option to block dynamic currency conversion DCC (Dynamic Currency Conversion) About half of domestic banks offer it. Thus, their customers can avoid unnecessary recalculations due to unfavorable exchange rates when paying by card at foreign merchants or withdrawing money from ATMs.

They provide customers with easy DCC protection Czech Savings Bank, Fio Bank, Mobile Banking, Partner Banks, Largest Bank and some (at ATMs only) Raiffeisen BankEven before this summer, other banks’ customers didn’t have such protections. Some banks didn’t do it, and some didn’t even want to do it.

Some ATMs or payment terminals abroad offer dynamic DCC conversion. This is almost always a disadvantage from the perspective of customers holding Czech payment cards. Foreign currencies are often converted into Czech crowns at a much worse exchange rate. Especially when paying in shops, people inadvertently use this “service” even though they are not interested in it.

Which banks can block DCC?

mBank was the first bank in the Czech Republic to allow its customers to prohibit unnecessary currency conversions (DCC) in spring 2020. Expobank (now Max Banka), Fio, Equa Bank (now part of Raiffeisenbank), Česká spořitelna and Raiffeisenbank gradually joined them. The new partner banks have also offered this option since their opening.

Customers of the above banks can easily and quickly block DCC in the way they set it, such as card limits or similar restrictions in e-banking. They can easily unblock it at any time – and also turn it on again later.

Raiffeisenbank, like Equa before it, only offers DCC limits for ATM withdrawals. It does not apply to merchant payments, where the risk of unnecessary use of DCC is greater – at least according to reader feedback and the experience of Peněz editors.

Setting up the card in electronic banking (DCC ban) is the most effective way for the customer to protect himself from services that he does not like to activate.

How to refuse DCC when withdrawing cash from an ATM?

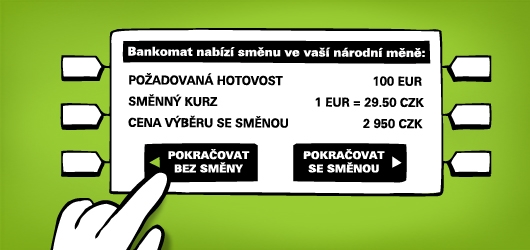

Unsolicited Dynamic Currency Conversion (DCC) offers are more likely to be rejected ATM withdrawalsIf the ATM offers DCC, you will have two options, one of which you must actively choose. In principle, the option without conversion is more advantageous, even if the ATM screen tries to intuitively guide you to the less advantageous option with conversion. Therefore, choose the button that shows the amount in the foreign currency instead of the button that shows the conversion in kroner.

Source: Aviation Bank

Source: Aviation BankDynamic currency conversion at an ATM. Go left, even if it’s not intuitive. (Image courtesy of Air Bank.)

Unfortunately, ATM operators are also responding to the growing awareness of their customers and the increasing likelihood of being blocked. Additional feesome local banks will ask for this information when withdrawing money from foreign cards.

Declining the DCC does not protect you from this fee – it’s usually “compensation” from the operator for not making money on the conversion. It doesn’t help if you have an account with a bank in your home country that doesn’t charge fees for foreign withdrawals. This is a fee that the card issuer cannot influence (or at least not directly).

ATM operators are required to inform you in advance of such fees and their amounts. If you disagree, do not withdraw anything from the ATM and try another machine nearby. Even in tourist areas (and more often outside of tourist areas), you can still find ATMs that do not charge customers for withdrawals.

Some card issuers in the Czech Republic (mBank, Fio and Max Banka) also allow customers to block this special fee. Even then, they have no choice but to try another nearby ATM.

How do I decline a DCC when paying at a store terminal?

At payment terminals in foreign stores, sometimes you simply don’t know that the seller has already selected the DCC option in advance. As a buyer, you automatically “agree” to this when you enter your PIN to confirm the payment, and the merchant himself rarely emphasizes to you in advance that he can earn a commission from the increased exchange rate. The merchant’s motivation to use this service in your own country is the same as their bank’s when they warn you abroad.

If you keep this in mind and check the details on the terminal, you will recognize the DCC by the fact that next to the amount in the local currency (e.g. Euro or Zloty), it also shows the conversion in kroner. This can be confusing, but remember: when abroad, you want to pay in the local currency, not “comfortably in kroner” – because the DCC exchange rate is often worse than the one your bank normally uses.

When you notice an unfavorable conversion, you can reject it and ask the seller to enter a regular payment in the terminal without a DCC. However, some shoppers may feel uncomfortable doing this due to language barriers or queues behind them. Also: it looks a little different every time, and when paying quickly, there may be cases where the additional information does not even appear on the terminal. If you only notice the unfavorable exchange rate later on the payment slip, your bank will usually not accept the claim because you have “agreed” to use a DCC.

Based on reader responses and editors’ experience, the situation seems to have improved over the past two years. Terminals – at least in more serious stores such as large fashion chains – usually give you a choice, so if you don’t confirm one of the two options, you won’t have any further options. Similarly, if you don’t want to make the usually disadvantageous DCC exchange, you should choose the local currency amount instead of the kroner.

Why do banks and merchants offer DCC? When can you benefit from it?

Serve Dynamic currency conversion (Dynamic Currency Conversion – DCC) was originally intended to make it easier for people to withdraw cash or pay abroad in the currency they are used to. For example, a tourist from Germany will see an amount in euros in addition to kronor in the Czech Republic. An immediate recalculation shows exactly what will be debited from his account – although it is usually much worse, it is guaranteed not to change again. In contrast, without DCC, payments are usually cleared within one to three days, so Today’s exchange rate It can get worse: or better. Although usually not by a significant jump.

European consumer organization BEUC has been arguing for years that the service has long lost its former theoretical advantages. In the second half of the 1990s, when DCC was created, it was not possible to immediately know the movements of one’s account. With the development of electronic banking, this situation has changed significantly. Since the abolition of roaming charges in the EU, it is no longer a problem to know the current exchange rate at any time.

Critics of the service argue that banks should activate DCC on the card only for customers who explicitly request this “service”. Alternatively, they should make it mandatory to allow people to block the conversion, just as they do by banning card payments on the Internet or setting various restrictions. However, such strict regulations are not incorporated into Czech law or EU regulation and therefore depend on the voluntary decision of individual banks.

A few years ago, some banks in the Czech Republic claimed that it was technically impossible to block DCC (the possibility of making customer settings on a specific card). He considered it his own point when the first competitors proposed such an option. Banks no longer use the former argument too much: the service can be advantageous. The banks in the Czech Republic themselves – as issuers of bank cards that their customers subsequently use abroad – have been warning their customers about this service in recent years, as has the Ministry of Finance.

However, in some cases, DCC is really beneficial. On the one hand, for those who cannot easily exchange amounts to kronor in countries with exotic currencies (thanks to DCC, they will see it on the display in advance). Or there is a risk that interest rates change quickly for the worse (thanks to DCC, the current rate is used – not the rate of two or three days from now). And the DCC markup is lower than the standard markup that banks use on cards.

However, the latter case (DCC is more advantageous than the standard rate) requires a more educated customer to make the comparison. But at the same time, a well-informed customer may not often use a card with an unfavorable exchange rate. Nevertheless: In previous years, I generally believed that The card with the worst domestic bank fee rate (Moneta, Raiffeisenbank) The ECB interest rate has increased by around 4%, and the markup when using DCC is usually higher.

Why do banks refuse to block DCC on cards?

As a result, even well-informed consumers often inadvertently use DCC to make unfavorable currency conversions. Why don’t banks protect their customers more effectively?

Some banks, such as Creditas and Komerční Bank, are planning to do so. Creditas spokeswoman Lucie Brunclíková confirmed: “We hope to launch this service when we merge Banka Creditas with Max Banka next year.” Komerční Bank spokeswoman Šárka Nevoralová said: “We have the option to block DCC from the services we offer to our customers in the future.”

Raiffeisenbank may also expand the current option – a ban on DCC at ATMs. “The main reason why we do not offer a blocking function at merchant payments is that we do not want customers to have the unpleasant experience of having their transaction rejected at the cash register. This prolongs the payment time, and the customer will not even realize that he has set up something like this (he will not link it) and will think that the card does not work. All this is under pressure due to long queues behind the customer,” explains spokeswoman Tereza Kaiseršotová.

“At the same time, we are seeing an increase in the number of terminals adopting DCC. We are therefore currently analyzing how popular this service will be with our customers. Depending on the results, we are ready to subsequently introduce DCC blocking on POS terminals,” added a Raiffeisenbank spokesperson.

On the contrary, Moneta, which calls itself a digital leader, rejects the possibility of a simple setting on the card. Mainly because people do not ask for such an option. “It proactively advises customers not to use the DCC service to withdraw cash. However, based on customer feedback from the branch network, contact center, complaints and feedback from our ombudsman, we do not have any interest in such a block,” said Lucie Leixnerová, a Moneta spokesperson.

Aviation Bank, which has proposed many customer-friendly innovations in the past, remains opposed. “At the moment, we have no plans to block DCC. It is a voluntary service and the customer must always actively agree to use it. Therefore, the customer does not make a choice without knowing it,” believes Michal Kuzmiak from the press department. The bank has also previously argued that the ATM or terminal may not have an Internet connection, so the customer does not have the option to unblock DCC on the spot. Or he simply does not remember that he blocked DCC and does not know why the payment did not go through.

Even UniCredit Bank has not yet provided an option to disable DCC cards.

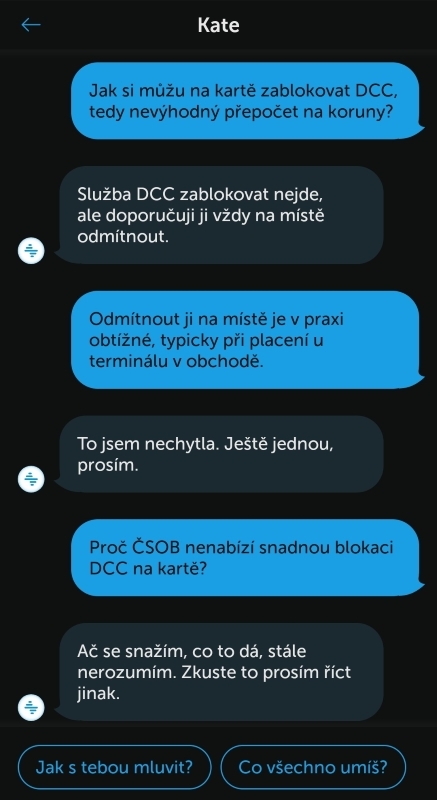

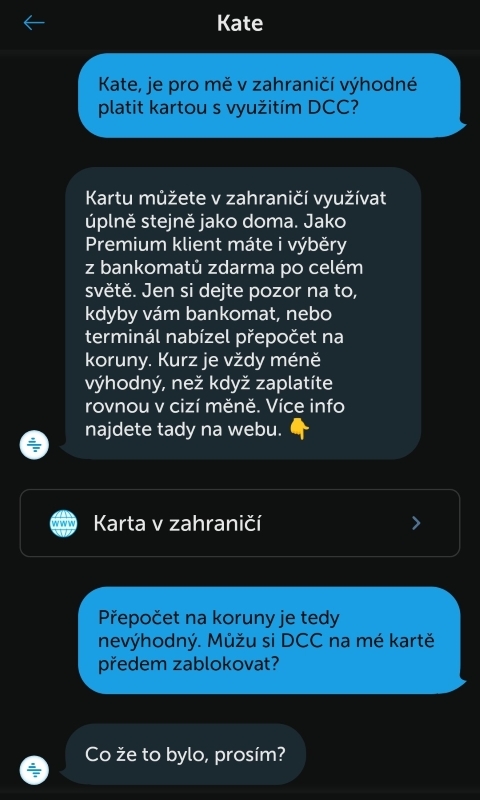

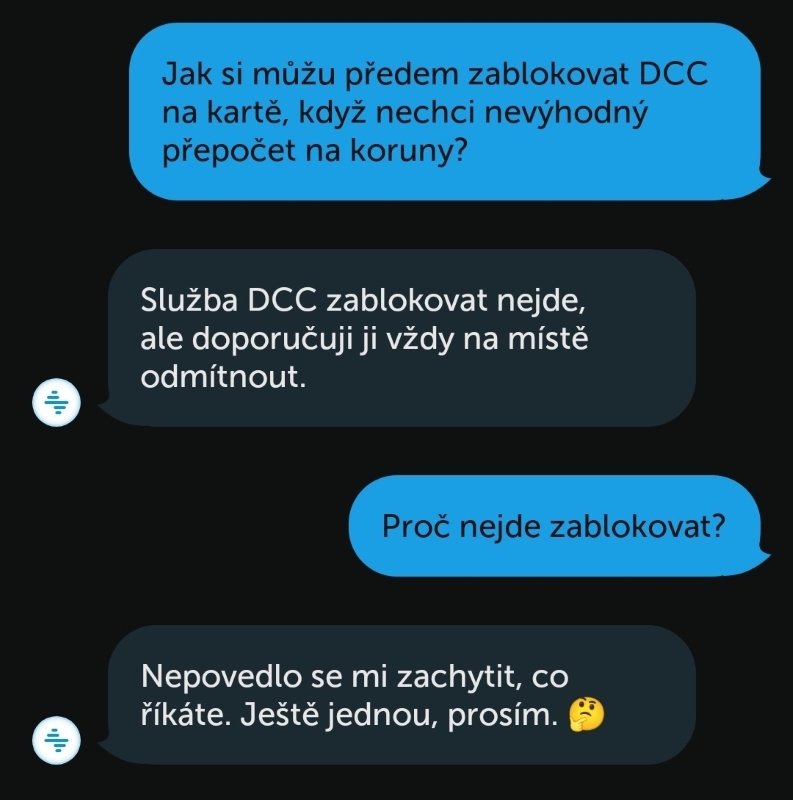

This summer, ČSOB customers will also have to live without simple protection. Its representatives did not answer questions from the Peníze.cz website. Unfortunately, even Kate, the bank’s vaunted virtual assistant, did not offer much advice to customers, as the following conversation shows.

Source: Peníze.cz, ČSOB mobile app

Source: Peníze.cz, ČSOB mobile app Source: Peníze.cz, ČSOB mobile app

Source: Peníze.cz, ČSOB mobile app Source: Peníze.cz, ČSOB mobile app

Source: Peníze.cz, ČSOB mobile appPeter Kucera

Share this before I delete the article

[ad_2]

Source link